March 19, 2018

Over thirty years ago, the responsibility of securing a comfortable life in retirement was up to the employers, not the employees. This is often known as the “Defined Benefit Era”. However, fast forward to today, and you will find that the responsibility has shifted as employees are now responsible to set themselves up for financial success. The problem with this model is often times employees use defined contribution plans such as 401(k)s or IRAs to fund their retirement which may be volatile and risky.

In this episode of Money Script Monday, Rob proposes a new approach to the way financial plans are structured that recreate the stability and income that was so popular during the Defined Benefit Era.

Video Transcription

Welcome to another episode of Money Script Monday. My name is Robert Reaburn. And today, we’re going to be talking about financial planning and some of the shortcomings that we notice with the traditional approach. Then, also look into history to see how can we improve the way we approach financial planning so that we can increase the amount of income security that we provide to each and every one of our clients.

To truly understand the mindset around a better financial planning approach, I always like to share the story of our founder, Bill Zimmerman, who said despite his great level of success, he never truly felt secure in retirement until he was able to utilize products and solutions that were able to provide income stability and then also income longevity.

In other words, he knew that no matter how long he lived, his income would never run out.

The question is in a defined contribution era that we live in today, how can we replicate the qualities of the defined benefit era that we noticed back before in 1980?

Let’s take a look at what a defined benefit plan looks like and then how we can get there.

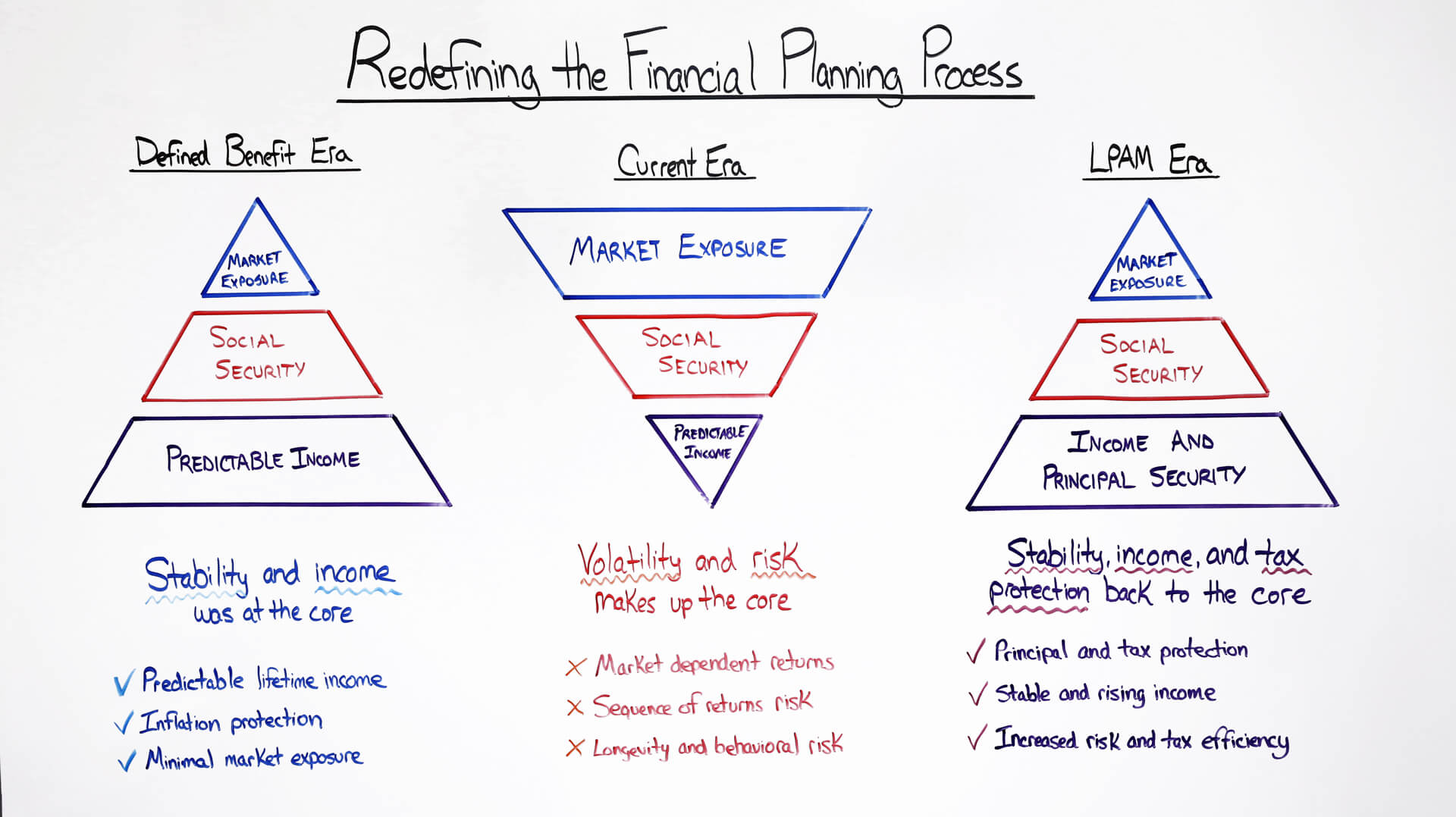

Defined Benefit Era

Prior to 1980, most Americans were under a defined benefit plan.

The great thing about these plans is it focused on the chief aspect that makes most clients insecure in retirement, which is predictable income generation.

Now, the risk was mostly on the company that the client worked for. The company had to make sure that those plans were funded so that they could pay their legal obligation to their clients.

For the clients, though, it was great, they had a level of predictable income that came from the company and they were able to enhance that income through the best and most formidable annuity we all know today, which is Social Security.

Then after that, any of those excess savings that clients built up over their lives, then they could put that into the market.

The great thing about that is no matter what the market did, clients knew that their lifestyle was secure through that predictable income from the defined benefit plan and that enhanced income from the government.

One of the things that we also liked about the defined benefit era is that it provided inflation protection as well. So, it didn’t matter how long you lived, that you were being punished for living a healthy lifestyle.

Something changed though. That was demographics.

Current Era

Americans grew older. They had less kids. So that meant defined benefit plans had less employees paying into these systems. And interest rates also dropped.

Companies really had a hard time funding these plans. What we saw over the next 30 years to today is that companies shifted to something called defined contribution plans.

And really, all that happened was the level of risk was shifted from the company to the clients.

Now, not surprisingly at all, that also coincided with the level of insecurity that Americans started to experience in retirement.

And why is that?

Because most, under today’s traditional approach, most of the risk, most of the reliance of retirement funding comes from the market itself, regardless if it’s the bond market or the stock market.

And when clients see their wealth fluctuating on a daily basis, that increases the amount of insecurity for their retirement.

The other problem with today’s current approach is that it doesn’t provide a predictable stream of income.

And that is very key. Even if the market goes up every single year, most clients are insecure when they know that every dollar they spend is going to decrease that finite amount of savings that they’ve accumulated throughout their entire life.

In other words, they are being punished if they live a healthier lifestyle.

And those who live an unhealthy lifestyle are being punished less so.

So, how can we even out the playing field? How can we make sure that clients are able to increase their income security?

LifePro Asset Management Era

Fortunately, there are products today that are affordable and reliable that can replicate all of those benefits that we enjoyed prior to 1980 into what we call the defined benefit era.

The goal today is, how can we recreate a defined benefit plan in the defined contribution era?

That’s where LifePro comes in and works with you, the advisor, and their clients to recreate those plans in a cost-efficient way and in a reliable and predictable way.

We want to shift the pyramid around where we’re reducing their market exposure and increasing the amount of income and principal security.

The way we create these plans is we use products that place stability, income, and tax efficiency back to the very core of everything that we do for our clients.

That allows us to increase principal and tax protection, so we’re looking for the products that replicate those values.

We also want to make sure that if clients live a long time, that we are accounting for inflation.

We want to make sure that we’re able to generate stable and rising income.

All of this sounds great, but how do we do it?

We start off with saying, “For every $1 that a client is saving, we want to make sure that we first focus on the products that secure that income and protect their principal in retirement.”

A lot of our advisors will first fully fund an IUL policy.

Then, enhance the income that an IUL generates through a fixed index annuity (FIA) product later on as clients’ approach retirement.

So, we’re able to say to a client, “If you need $100,000 to maintain your lifestyle through a combination of IUL funding, fixed index annuity funding later on in life, and then Social Security, in many cases, we can get you 90% to 100% of what you need in retirement through income that is both predictable and protects your principal.”

And that is something that really brings smiles to a lot of clients’ faces.

Here’s the other reason why that’s great.

For those excess savings that a client has, they can now focus on utilizing the market the correct way, which is not to provide protection or income, but to grow their asset base.

Because that’s really what the market is the best for is we want to invest in good companies that are going to grow over the long-term and deliver value to their clients.

But if they’re relying on the market for most of their savings, the reality is they’re going to get shaken out by the volatility of the day-to-day moves of the market when they should actually be putting more money into the market on those down days.

We think that creating this defined benefit plan for the defined contribution era through life insurance and annuities can really help a client not only secure their income, but actually deliver a more risk-efficient overall return strategy for their portfolio in retirement.

Contact LifePro Asset Management

Thank you for your time. And if you have any questions, please feel free to contact us by phone at 1-888-LIFEPRO (543-3776) and we can walk you through these plans, how to construct them and how to implement them. Thank you and have a great day.