July 7, 2017

Approaching retirement soon?

If so, your investment portfolio may be heavily invested in either government and/or investment grade corporate bonds.

With the recent rise in interest rates, you may want to consider alternatives that hedge the risk posed by bonds in this environment.

In today’s episode of Money Script Monday, Rob presents a solution that successfully replicates the objectives of a fixed income portfolio while taking into account possible liquidity needs for you and your family.

Thankful Yet Vigilant

Welcome to another episode of “Money Script Monday.” My name is Rob Reaburn, and today we’re going to be talking about “A Better Alternative to Bonds During a Rising Interest Rate Environment.”

Now, you might be asking yourselves, “Why are we talking about this topic today?” And the primary reason is that we think there is a danger lurking for a lot of investors out there right now, and that is the danger from rising interest rates.

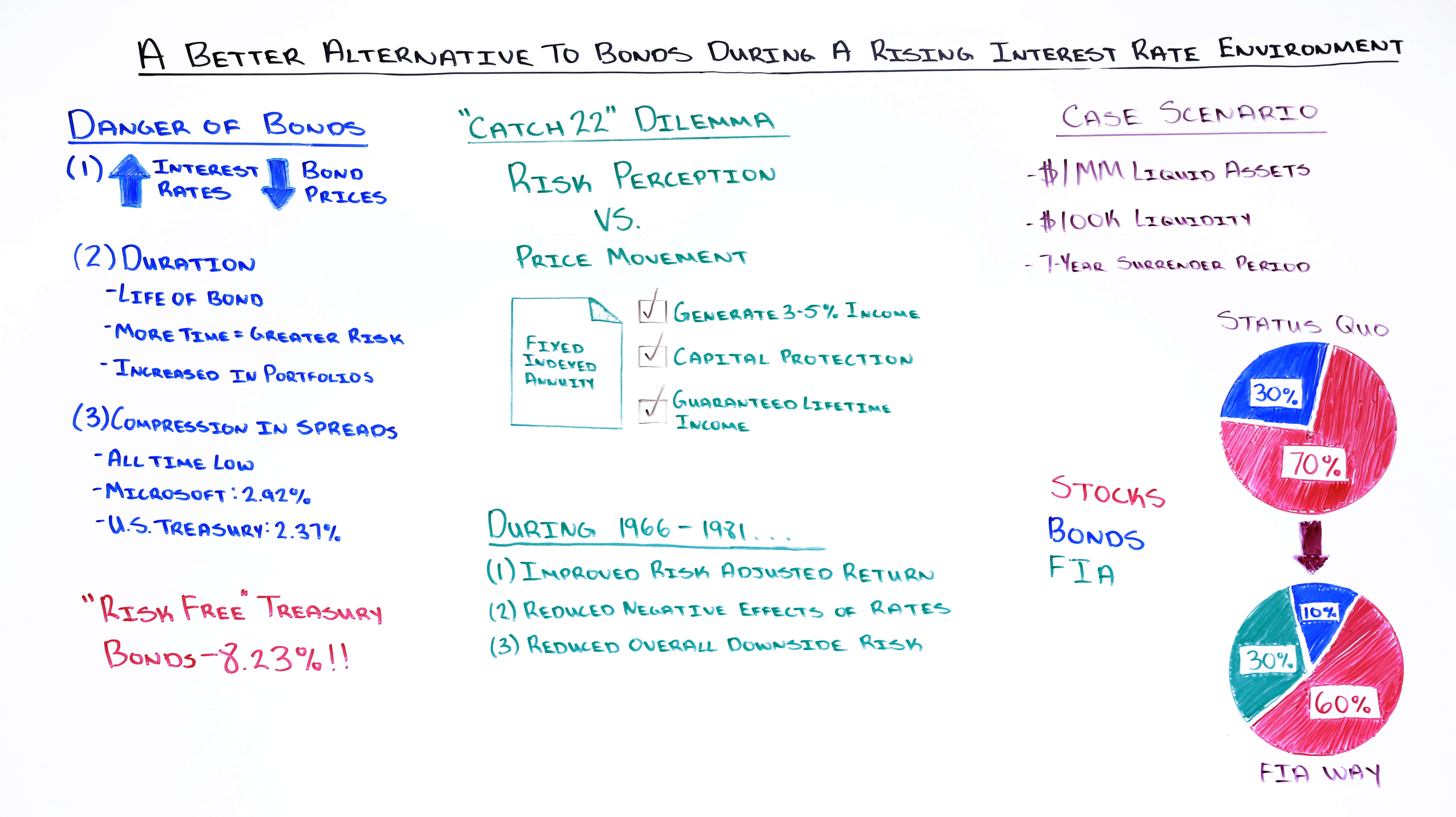

Danger of Bonds

We all know that interest rates only go in one direction, and that’s lower; this has been the case for 30 years.

But the truth is that the bond market actually moves in both directions, and typically moves in what we call “30-year interest rate cycles.”

Back in 2012, we believed that we started to exit from the current 30-year interest rate cycle that has exhibited lower interest rates.

(1) Interest Rates and Bond Prices

(2) Duration

The main danger that comes from investing with either a corporate bond or a government bond is the credit risk. So in other words, if we own a corporate bond, will that company be around in ten years?

Most of us that have a lower risk tolerance would be mostly focused on investment-grade bonds.

That means companies that are blue chip, very well-run companies where that really isn’t a huge risk.

The other risk comes when interest rates increase, the price of the bond comes down.

In other words, investors are not as willing to pay for a certain set of cash flows that interest rates are increasing because the value of those cash flows is going down as interest rates increase.

This can all be encapsulated with something called “duration.” Duration simply means “the life of the bond.”

So if you buy a bond that is going to mature in ten years, in general, the duration of that bond will be around ten years. Now, if you own it for five years and there’s five years left on that bond, that duration is going to be about five years.

This is important because the more time that there’s left on a bond, the more interest rate risk there is. The second reason why it’s important is as interest rates have decreased, the duration on a lot of bond funds has increased.

And that’s because portfolio managers have to be able to maintain that income that you enjoy today on those bond funds, and the only way to do that is by to increase the life of the overall portfolio.

In other words, they have to buy a ten-year bond to get 3% versus a five-year bond that would have generated 3% ten years ago. This is increasing the overall level of interest rate risk that you are exposed to in your investments.

(3) Compression of Spread

The other reason that there is pent-up risk in a lot of these bond funds is because we’ve seen what’s called a “Compression in Corporate Spreads.”

In other words, Microsoft today yields 2.92% versus the U.S. Treasury at 2.37%. That spread between 2.92 and 2.37 is the premium that investors charge a corporate client to lend money, to borrow money, versus the U.S. government.

That’s at an all-time low.

In other words, we’re not going to be able to generate a lot of return for investors based on the improving corporate credit profile. Which means we have to rely on interest rates going lower for the price of the bond to move up.

And given that we’re at an all-time low in interest rates, you do the math. The chances are that we’re not going to generate a lot of return on the bond from the price itself.

So we’re really only left with getting the yield.

And as most of us know, the yields on bonds right now are just not sufficient to cover our living needs.

So we have to ask ourselves, “Is there a better alternative?”

Should we go into government bonds?

Because those are risk-free, right?

Not so fast.

Yes, it is correct that U.S. Treasury bonds are risk-free. But the problem is they are exposed to interest rate risk.

Last fall, when the new administration came into power, the U.S. seven to ten-year bonds sold off 8.23% in a matter of months.

"Catch 22" Dilemma

I would ask those at home that are watching this right now, can you tolerate an 8.23% loss in a matter of months on those assets that are supposed to be safe?

This is supposed to be helping you fund your retirement?

The answer is probably no.

You’re probably saying, “That’s great, Rob. What is the alternative? I’m not going to go into stocks, am I?”

And that’s the Catch 22, Risk Perception versus Price Movement.

We’ve all been taught that bonds are less risky than stocks in retirement, and that as we approach retirement, we need to increase our bond exposure.

We know that we can’t go into stocks because stocks, regardless, are always going to be more volatile than bonds. If bonds are not the place to be, what’s the alternative?

There is an alternative and we believe it’s called the Fixed Index Annuity.

And the truth of the matter is when we look at what our bond portfolio is supposed to be doing, we’re hoping that it does all three of these things.

The only difference is that we’re not exposing ourselves to downside risk, and we’re getting a guarantee from the carrier.

During 1966 – 1981…

The next question you might ask is “Well, that’s a theory. Can you prove it?” And we can, and we back-tested these strategies and said, “How do Fixed Index Annuities work in a long-term environment of rising interest rates?”

Fortunately, we had a period to test that, and that was from 1966 to 1981. We said, “What if replaced all of a client’s bond allocation into a Fixed Index Annuity? What would that do for the overall return profile of their retirement plan?”

What we found is that by increasing a client’s Fixed Index Annuity exposure, we were able to improve the risk adjusted return of the overall retirement portfolio, we also reduced the negative effects of rising interest rates.

In fact, we benefited from rising interest rates because as interest rates increase, the amount of interest that annuities were generating went up.

So as we reduced our equity exposure, our stock exposure, we actually had a higher blended rate from those annuities. We reduced the overall downside risk of the portfolio because while bonds were selling off 5 to 10 to 15%, our portfolios were doing nothing because the downside is guaranteed.

That’s the primary benefit that we can get.

Case Scenario

This particular gentleman, we’ll call him “Jim”, has a household that has about $1 million in liquid assets, but they have about 70% in stocks; he’s 55 years old and 30% in bonds.

That’s great, but he’s got a little too much exposure to stocks at his age and that bond portion, as we’re entering a rising interest rate environment, is a little risky.

How do we implement a Fixed Index Annuity strategy into this portfolio?

It’s simple.

We want to make sure that we’re addressing the liquidity needs of our clients.

In this case, Jim needs about $100,000 of liquid cash that he can access at any time. For that $100,000, that’s the $100,000 that we’re going keep into bonds.

The rest of the cash, in this case, the other 30%, is going to go into a Fixed Index Annuity, while the remainder, the 60%, will be in stocks.

The good thing about this setup is the 60% will slowly draw down and the fixed index annuity portion will slowly increase.

And what that means is that once we’ve made the change, over 30% of this investor’s portfolio will never go down in price. Versus before, when the 100% of the portfolio was exposed to downside exposure.

So taking an easy step of reducing our bond exposure, increasing our exposure to Fixed Index Annuities with the right tools can dramatically reduce your overall risk of your retirement portfolio while maintaining the income you need in retirement and also providing that guarantee of lifetime income and helping you sleep more soundly at night.

Thank you and have a wonderful day.