June 18, 2018

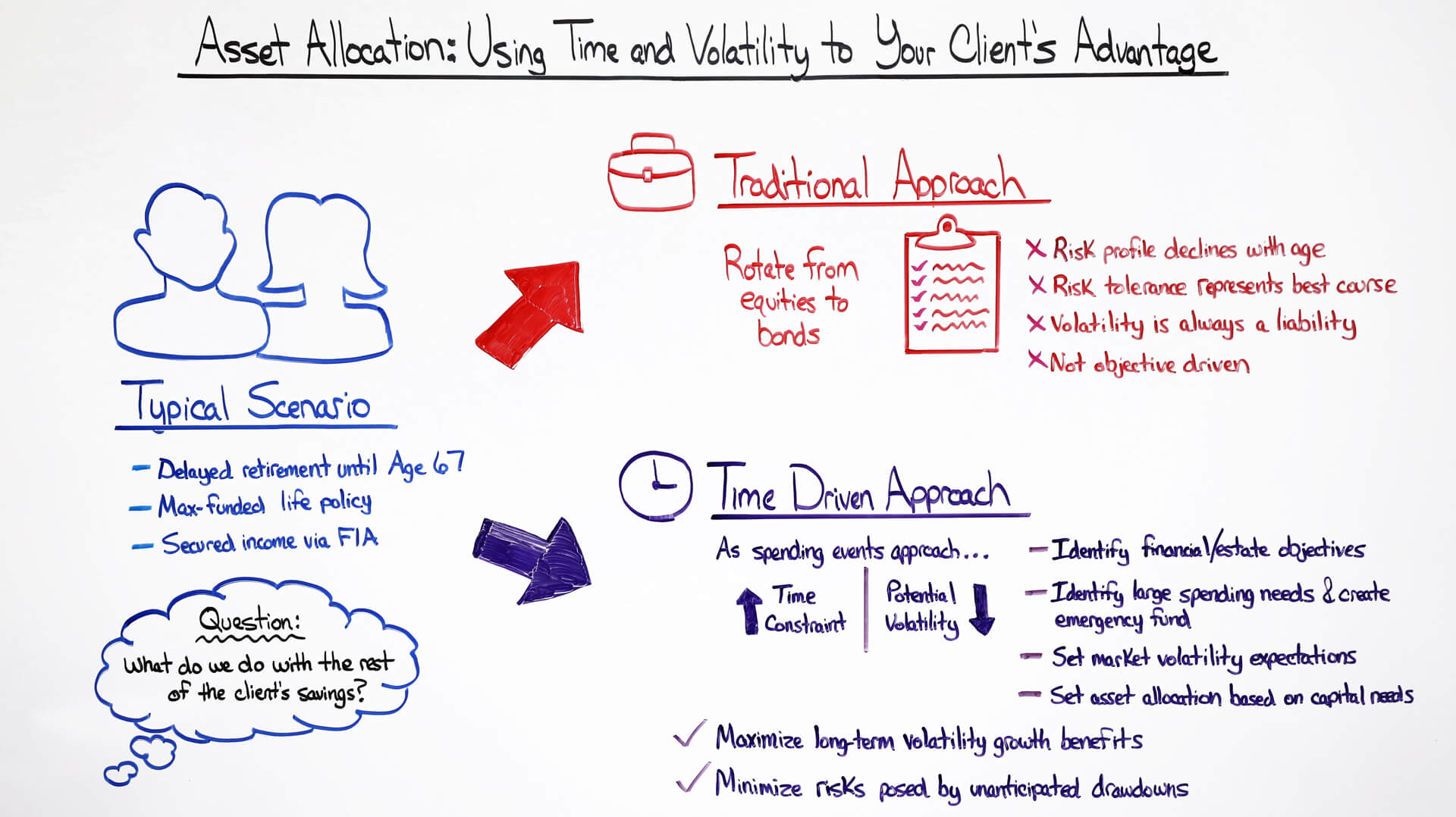

The traditional approach of asset allocation relies heavily on emotional responses to risk tolerance surveys and the idea that market volatility is always a liability. But, what if you could use volatility to your client’s advantage? In this episode of Money Script Monday, Robert explains how to use a time driven approach to identify your client’s financial goals and maximize their growth potential.

Video Transcription

Hi. My name is Robert Reaburn and welcome to another episode of Money Script Monday.

Today, we’re going to be talking about how you, the advisor, can use both time and volatility to your client’s advantage.

Ultimately, what we want to get out of today’s presentation is to really illustrate to you, the advisor, an alternative approach to asset allocation, that is more driven based on the client’s objectives and their long-term spending needs.

In prior episodes, what we talked about in terms of asset allocation, was really focused on a three-step process.

Which was discovering the client’s needs, securing the client’s lifestyle in retirement by using life insurance strategies, annuities, and of course, maximizing the amount of income that we can acquire through Social Security.

Now, all of that is great, but it still begs the question, what do we do with the surplus part of that equation?

What do we do on that third stage?

Traditional Approach

For 99 out of 100 advisors today and their clients, they’ve really relied upon the more traditional approach to investment allocation, which is based on risk tolerance surveys.

We’re going to talk a little bit why this is a flawed approach.

Especially in an environment where we’re seeing long term interest rates beginning to increase, and we may be very well entering a new 30-year cycle of rising interest rates.

The traditional approach simply states that over time, as we approach retirement, we need to decline the weight of equities and we need to increase the amount of money we have invested in bonds.

Secondly, the ultimate risk profile continues to decline with age, regardless of what the objectives of our clients is.

And then of course, that finding out a risk tolerance number is the best way to figure out what that client needs to be invested in.

Now, we’re going to walk through why that is truly a flawed approach, and that it’s quite frankly, emotionally driven.

And then lastly, that volatility is always a liability.

When we think of risk profile surveys, the problem really comes down to what these risk survey, the input, which is what the client is answering these questions.

The real problem there is that it’s driven by a client’s emotions, and when we think of the most robust types of financial planning methods, we want to take emotion out of the process.

We want to figure out long term, what are the objectives of the clients, and what are the spending needs of the clients.

In other words, what are those liquidity needs the client needs in the short term and ensuring that we have the client invested in assets that does not jeopardize short term spending needs and maximizes the chances that we’re going to succeed in achieving those client’s long-term objectives.

So, how do we get there?

How do we actually get to that approach?

The first step is to realize that volatility is neither a liability, nor an asset.

It’s really both. It really goes back to when does the client need their money.

Time Driven Approach

This gets us back to our time driven asset allocation approach.

This is the method that we have studied and the method that we believe really removes the maximum amount of emotion out of the asset allocation process, and really brings the client’s objectives, both in the short term and the long term, to the surface.

So, how does it actually work?

To really simply speak, as a spending event approaches for the client in the short term, the amount of time constraint goes up, which means the amount of volatility within those bucket of assets that are needed in the short term, comes down.

Now here’s why.

One of the risks that a lot of our clients are exposed to is sequence of return risk.

Sequence of return risk is mostly focused in the short term. So, as a spending event approaches, we want to reduce the amount of sequence of return risk that our clients are exposed to.

In the long term however, sequence of return risk decreases as a factor and as a danger to our client’s assets.

In other words, volatility goes from being a sequence of return risk, to really being a growth asset, because growth and volatility are correlated to each other.

In other words, growth assets tend to be more volatile.

And so, the longer our time horizon is, the more our clients can take advantage of the growth advantages that a more volatile asset possesses.

What we want to do is, when we approach a client, we want to discover what are those spending needs that a client needs in the next one to two years, two to four years, and really four years and beyond.

The reason why we use those time buckets of one to two years, two to four years, and four years and beyond is that we know that historically speaking, the market has certain recovery rates after certain draw down periods.

We want to match the draw down periods with products that have relatively the same draw down profiles.

So, if we have a client that doesn’t have a spending need for the next four years plus, we want to put them into a growth product that we know, even if the S&P 500 goes down 40%, on average we can get back to break even within 4.2 years, and not jeopardize a spending need that that client needs before then.

What happens if you do have a client that has a spending need in the next one to two years, they’re in a growth asset, but they also have a high-risk number.

This is where our time driven approach really sets you apart.

Over time, as a spending event approaches, regardless of how risk tolerant your client is, we’re going to be taking those assets out of the more growth focused vehicles and into a more capital preservation focused investment solution.

We know on those capital preservation assets, that even if the market goes down, the average draw down will only really be 4 to 8% and the average recovery period for those assets is also within the one to two year time bucket.

That really allows the client to sleep better at night.

Once we’ve done that, we always want to set up what we call an emergency fund.

In other words, outside of our income vehicles, do we have an emergency fund that if an unanticipated spending event comes up for our clients, they will be able to draw from that money and know that it’s really not going to fluctuate based on the market.

So, if we can set up an emergency fund that is adequate to meet some emergency large scale spending needs in the short term.

Then allocate the rest of our client’s assets based on the long-term spending profile that the client and you have put together.

We believe that those types of plans that are objective driven and focused on spending needs, will really be able to maximize the amount of risk adjusted return that we can generate for our clients.

If this is an approach that sounds interesting to both you and your clients, we’ve put together some tools that will really help simplify the whole discovery process, and then allocate those assets based on the long-term spending needs for your clients, and of course, their objectives.

Contact LifePro Asset Management

Thank you again for your time and have a wonderful day, and if any of us can provide assistance to you please feel free to reach out to myself or anyone else here at LifePro at 1-888-LIFEPRO (543-3776).

We’d be more than glad to assist you. Thanks again and have a wonderful day.